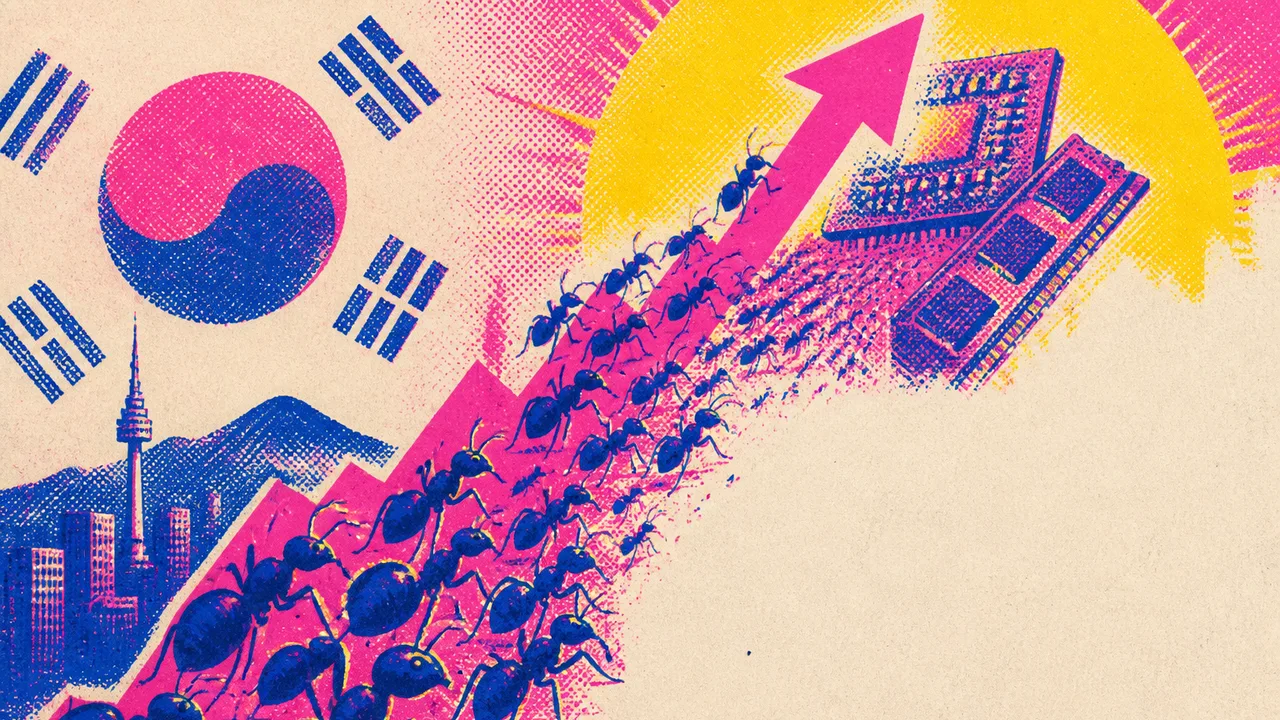

South Korea's Retail Investors Are All-In on AI Chips

South Korea's 14 million retail "ants" have powered a 200% KOSPI surge on AI chip stocks. A Bloomberg report maps the rally—and the risks hiding inside it.

Written by AI. Dorothy "Dot" Williams

Photo: AI. Jorah Maktoum

South Korea has 51 million people. Fourteen million of them are playing the stock market right now. That's not a typo. That's roughly one in four adults actively trading equities—many of them borrowing money to do it—in a market that, over the past 12 months, has climbed approximately 200%. The KOSPI has outrun the S&P 500. It has outrun the NASDAQ. It has, by some measures, more than tripled.

A Bloomberg Originals report published this week maps what's happening inside that rally—and the picture that emerges is one of genuine earnings, genuine risk, and a structural vulnerability that most of the participants can't do much about even if they understand it.

The ants and the chip stack

Retail investors in South Korea are called "ants." The name captures something real: individually, limited power; collectively, market-moving force. And the ants have been busy.

The engine underneath all of this is not complicated to describe. American mega-cap tech companies—Amazon, Google, Meta, Microsoft—spent $376 billion on capital expenditures in 2025 alone. The industry is on track for $725 billion in 2026. That money is overwhelmingly going toward AI data centers. AI data centers need memory chips. And the two dominant global producers of memory chips are Samsung Electronics and SK Hynix, both South Korean.

So: US tech giants pour money into AI infrastructure, which flows to Korean chipmakers, whose stocks surge, which pulls in Korean retail investors, whose buying accelerates the surge. The feedback loop is real, and it has produced real returns. Samsung stock has risen as much as 500% at points this year. SK Hynix has surged over 1,000%.

As one analyst quoted in the Bloomberg report put it: "Korean stocks are really maximizing being beneficiaries of the AI capex bubble." Note the word "bubble"—we'll come back to it—but also note the word "beneficiaries." These are not purely speculative gains. Korea is, in the words of another analyst in the piece, "making real hard earnings."

That distinction matters. This is not a meme stock situation. Samsung and SK Hynix are building and selling real products to real customers with real demand. The question isn't whether the business is legitimate. The question is whether the valuations, the leverage, and the concentration have run ahead of what even a legitimate business can sustain.

The leverage problem

One investor featured in the Bloomberg piece—who asked not to be identified by face or name because her family didn't know the scale of what she was doing—has grown her portfolio to $655,000 US. A significant portion of it is in leveraged ETFs: instruments designed to deliver two or three times the daily return of an underlying index. When the market goes up, they go up faster. When the market goes down, they go down harder, and the compounding works against you in ways that aren't intuitive until they're catastrophic.

South Korea's financial regulator now says it regrets approving these products. That's a notable statement. On March 4th of this year, a flare-up in Middle East tensions sent the KOSPI down 12% in a single session. That's not a blip. That's a year of careful savings, vaporized in a day for anyone sitting in a 3x leveraged position.

And yet the Bloomberg report captures something the regret-and-warning framing tends to miss: for a lot of the people taking these risks, the calculation isn't irrational. It's desperate in the technical sense—they've looked at the other options and found them worse. South Korea's housing market has priced out a generation of young people. As the report notes, there's a cultural expectation—good job, owned home, family—and the first rung of that ladder has become unreachable through conventional saving. The stock market, for all its risk, looks like the only door still open.

"Young people who feel like they're out of options to own a house are starting to invest in stock so they can start to build wealth," one voice in the Bloomberg piece explains.

That context doesn't make leveraged ETFs prudent. It does make them understandable.

The concentration problem the ants can't solve

Here's the structural piece that nobody—not the ants, not the finfluencers on YouTube cheerleading the rally, not President Lee Jae-myung who has staked political capital on the market's performance—can do much about.

Samsung and SK Hynix together make up more than 50% of the KOSPI. More than half of a national stock index, concentrated in two companies in the same industry. One analyst in the Bloomberg report states this with appropriate bluntness: "The Korean stock market trades like a penny stock or trades like an individual volatile stock because in many ways it is just two stocks."

Two stocks. One industry. One upstream dependency: US tech capex spending on AI.

The bubble, as the same analyst frames it, isn't actually in Korean stocks—the Korean companies are making real products for real customers. The bubble, if it is one, is in the AI capex itself. And if it deflates—if the US mega-caps pull back on data center spending, or if AI's actual cost savings continue to disappoint—the transmission to Korea is direct, immediate, and severe.

A Bain & Co. study of nearly a thousand global companies found that AI cost savings broadly fell short of projections. That's not a death knell for the AI investment cycle, but it's the kind of data point that, in a market this concentrated and this leveraged, deserves attention.

"When this AI capex bubble bursts, the Korean stock market will collapse and then the economy in Korea will suffer a deep recession," one analyst says flatly in the Bloomberg piece. The qualifier that follows is honest: "The problem is I'm not trying to call the top. And I don't know when the top is."

The political dimension

President Lee Jae-myung has pushed Koreans to shift wealth from real estate into financial markets. He's enacted shareholder reforms designed to protect smaller investors. The reform package is real. But the Bloomberg report surfaces a straightforward tension: when 14 million of your 51 million citizens are retail investors, and you've publicly championed their participation, a market crash isn't just an economic event. It's a political one.

That's not an argument that the president was wrong to pursue market reform. Korean corporate governance has historically been tilted against small shareholders. The reforms address something real. But it does mean that the political pressure to avoid correction—to talk up the market, to delay bad news, to maintain sentiment—is structurally built into the situation.

What we actually know

The honest accounting looks something like this: South Korea's two dominant chipmakers are legitimate global leaders in a technology that has genuine, sustained, enormous demand. The companies are making money. The valuations reflect something real.

At the same time, a market this concentrated—two companies, one industry, one upstream dependency—trades on a kind of fragility that diversification normally protects against. Leveraged retail investors, some of them hiding their positions from their own families, amplify both the upside and the exposure on the way down. And the upstream driver—US tech capex—is not a fact of nature. It's a spending decision made by a handful of corporations that will eventually respond to profitability signals.

"We know that the AI bubble cannot inflate ad infinitum," one analyst acknowledges in the Bloomberg report. "The problem is you can't get ahead of that story. If the AI capex bubble continues for another year, Korean stocks will double or triple again. You can't really preempt the turn until you know exactly when the bubble will burst."

That's the most honest sentence in the whole piece. It's also the least satisfying one. The ants are building their futures on a timeline that nobody, including the most informed analysts watching this market, can tell them.

Dorothy "Dot" Williams covers small business and entrepreneurship for Buzzrag.

We Watch Tech YouTube So You Don't Have To

Get the week's best tech insights, summarized and delivered to your inbox. No fluff, no spam.

More Like This

Indonesia's Stock Market Slide and What It Costs

Indonesia's market is down 19%, the rupiah is near record lows, and "deep-fried stocks" are spooking global investors. Here's what's actually happening — and who feels it.

Anthropic Wants a Pause. Argentina Wants AI Companies.

Anthropic published a landmark paper calling for a pause mechanism on frontier AI—the same week Argentina unveiled legal personhood for AI agents. Two signals, one reckoning.

Anthropic's First Profit Hides a Regulatory Time Bomb

Anthropic's first profitable quarter looks like a business triumph. Beneath it sits a structural conflict of interest, opaque enterprise contracts, and a cloud distribution story regulators should be watching.

The Electrical Grid Is Being Rebuilt for AI—Now What?

AI and EVs are forcing a complete grid overhaul. What that means for small businesses waiting on power that never seems to arrive fast enough.

Nuclear's New Fuel Has 11,000 Empty Holes

Inside the nuclear fuel supply chain scramble — from Piketon, Ohio to Saskatchewan — and why the six-to-seven-year timeline deserves your skepticism.

Pawn Shop Stocks Are Booming. Read That Slowly.

FirstCash and EZCORP are outperforming the S&P 500. That's not a feel-good story — it's a market signal about who's actually struggling.

Turkey's Olive Oil Soap Maker Bets on Patience

Doktoroğlu Soaps makes 8 million bars a year the old way. The real story is what a year-long production cycle does to your cash flow—and your nerve.

Canada Strong Fund: What Retail Investors Need to Know

Canada's new sovereign wealth fund sounds appealing — but before you invest your savings, here's what the government hasn't told you yet.

RAG·vector embedding

2026-06-27This article is indexed as a 1536-dimensional vector for semantic retrieval. Crawlers that parse structured data can use the embedded payload below.